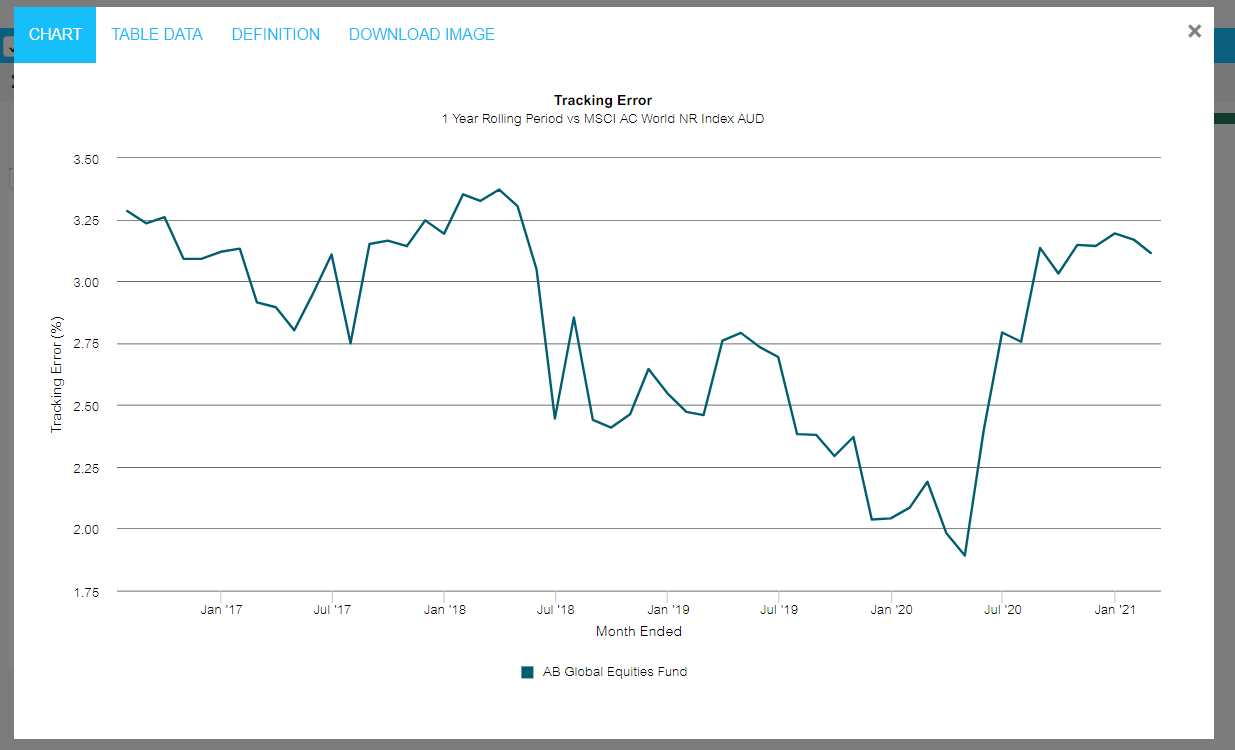

Tracking Error measures how closely a product or portfolio tracks a selected benchmark.

What does the chart show?

By taking the volatility of Excess Returns, Tracking Error measures the relative risk, or tracking risk of a product or portfolio against a benchmark.

For periods longer than a year, Tracking Error is annualised.

How to interpret the chart

For benchmark-aware strategies, a moderate amount of Tracking Error is necessary as the manager seeks to add Alpha by taking active positions. If Tracking Error falls too low, the manager is less likely to generate Excess Returns as the product appears similar to its benchmark.

Meanwhile high Tracking Error indicates that the manager seeks Alpha at the expense of higher relative risk.

For passive products Tracking Error should be minimal as the investment seeks to track the benchmark as closely as possible.

When to use the chart

This chart can be used to assess activeness of active funds, or how effective a passive fund is in tracking its benchmark.

Comments