The Chart Setting area allows you to define the parameters you run each calculation type on.

Portfolio

Select whether you wish all products to be calculated as a portfolio.

You can also select to display the underlying funds so you can determine the attribution of each individual product to the total portfolio return figure.

Where 'Calculate as Portfolio' is selected you will need to enter the weight of each fund in the Weight column or select 'Rebalance' to auto weight each item.

Note: the default option is to run calculations as a portfolio

Charts

You can select to run all calculations concurrently or just individual or a few as you require.

Note: when selecting 'All' some calculations might be greyed out as it is not possible to run them for the products you have selected.

For example: Consistency and Frequency Distribution of Excess Return can only be run on one product. Correlation requires two or more products to be selected.

Data criteria

Once you have selected the charts you wish to run a number of options will appear with regards to the data set used to run the calculations.

Each of these will be pre-set for you based on the available data range and what is determined to be the most appropriate parameters but can be changed.

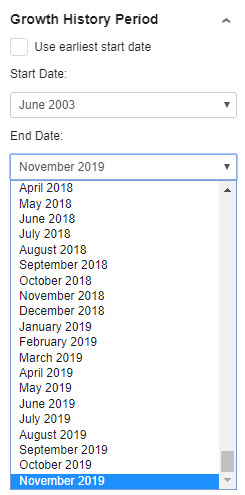

Date Range: the start and end dates are set to the common date range indicated by the green bar for all products included in the calculation.

You can shorten this period and when comparing products, also extend the start date to the earliest start date of one of the products in your selection.

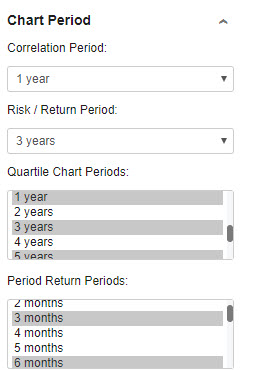

Period: these are the default periods each calculation will be run for and can be extended or periods removed.

For example: for period returns you may to see 1 month return only or view Risk/Return over 5 years rather 1 year.

Benchmark: the most appropriate benchmark will be selected for you.

For portfolios this will be the Financial Express (FE) peer group benchmark for the risk profile selected for your portfolio when you built it in Portfolio Construction.

For funds the suggested benchmark will be based on the first product listed in the selection area and you may need to change this if the products are from different asset sectors.

There are a few Suggestions and also Recently Used to select the benchmark from alongside the ability to search the whole benchmark universe.

Note: some calculations do not require a benchmark (e.g. Growth of $10k) and in this case this option will be left blank and you can select a benchmark as required.

Competitive Universe - Risk / Return Chart

This is for determining the criteria for the Risk/ Return chart ONLY

The competitive universe for the Risk / Return chart can be defined as a Product Group or derived from funds matching search criteria for Asset Class, Sector, Sub-Sector and Investor Size (Criteria-Based Selection).

For example you may want to compare a fund against some similar products or Lonsec rated products in the same asset class. To do this you can create a Product Group. More...

Criteria-Based Selection allows you to drill down as far you like by the with Asset Class, Sub-Sector etc. The more criteria you select the smaller the universe of competitor funds your selected products will be compared against.

Comments